Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The way in which capital gains of a fund are allocated between the participants in an investment

A distribution waterfall is a popular term in equity investing that refers to how capital gains from a fund are allocated among participants, typically the limited partners (LPs) and the general partner (GP).

The capital of limited partners is managed by the general partner in a private equity fund. The general partner himself contributes a relatively small proportion of the total investment.

Distribution waterfall structures are put in place primarily to ensure that profits are allocated to the manager only after the limited partners have received the agreed return on their investment. The structures are detailed in the distribution section of the private placement memorandum (PPM).

A distribution waterfall lays down the rules and procedures for the distribution of profits in a private equity investment agreement. Its main purpose is to align incentives for the general partner and define a pay structure for limited partners.

The distribution structure can be visualized as a set of buckets placed one below the other. Each bucket defines an allocation of profits. When the first bucket is filled to the brim, the profits flow into the second bucket, and so on.

In such a manner, the capital flows from limited partners (favored by the initial buckets) to the general partner (favored by buckets further away from the source). Such a structure of allocation protects the interests of the investors and, at the same time, incentivizes the general partner to maximize the return of the fund.

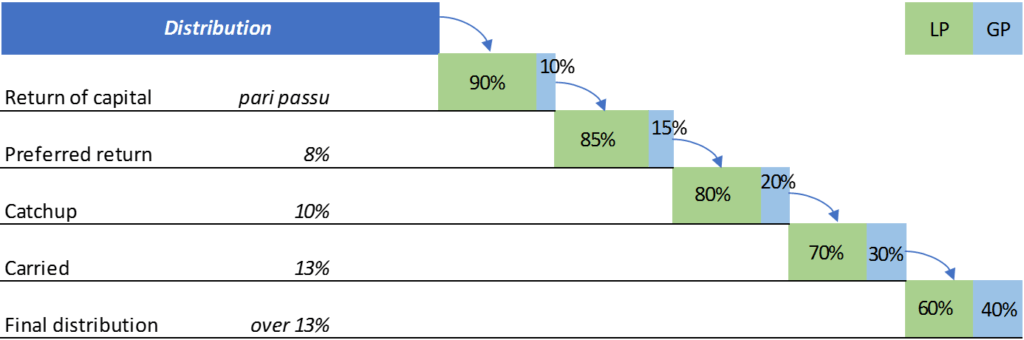

The allocation in question derives its name from the cascading nature of its four constituent tiers, which are shown below.

In addition, the hurdle rate, which is the minimum rate of return on an investment required by an investor, can be another tier. In case an excessive incentive fee is given to the manager or general partner, a “clawback” clause in the PPM mandates the return of such excess fees.

The four tiers are:

Return of Capital: The initial capital investments of investors, plus some expenses and fees, are returned to them.

Preferred Return: 100% of the distribution goes to the LPs until the preferred internal rate of return based on every distribution to them and every contribution called is reached.

Catch-Up: The catch-up bucket is highly favorable to the general partner. They are given all or a major portion of the gain until they receive a certain percentage of profits.

Carried Interest: It constitutes the allocation of the remaining amount between the limited and general partners.

Here is a side-by-side comparison of European Waterfall distribution vs American Waterfall distribution:

| Application Level | Applied at the aggregate fund level. | Applied on a deal-by-deal basis. |

| Priority of Distributions | Investors (LPs) receive return of capital and preferred return before the GP receives profit share. | General Partner (GP) can receive profit share earlier from individual deals. |

| Investor vs. GP Advantage | More investor-friendly. | More GP-friendly. |

| Manager Incentives | Managers may receive carried interest later, potentially reducing short-term motivation to maximize returns. | Managers can receive carry earlier, providing stronger short-term incentives. |

| Risk Mitigation Mechanism | Not typically highlighted because investors are paid first. | Often includes a clawback clause requiring the GP to return excess carry if overall fund performance later declines. |

| Main Drawback | Potential manager demotivation due to delayed compensation. | Higher risk to investors unless protected by clawback provisions. |

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI offers the Capital Markets & Securities Analyst (CMSA)® certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: