Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

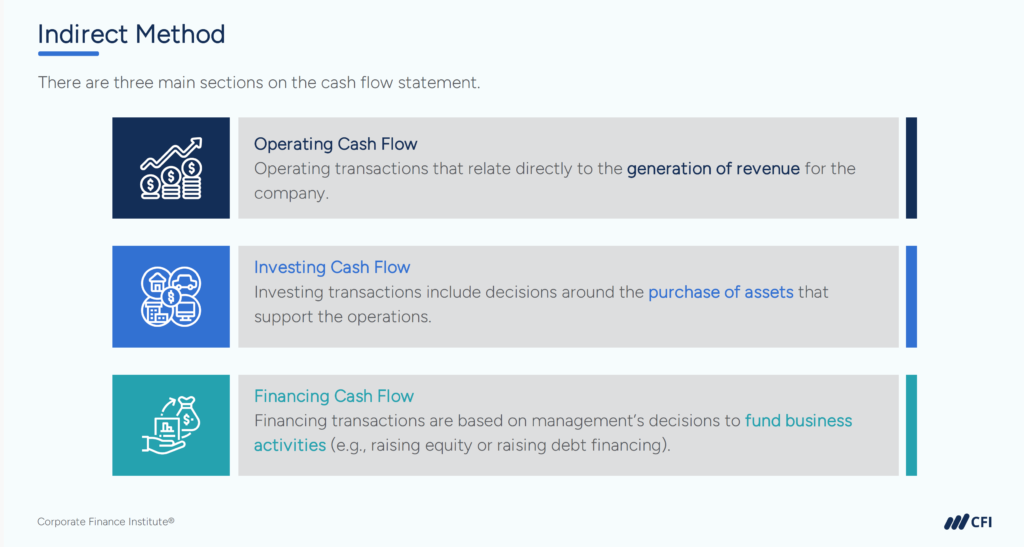

The indirect method is a standard accounting technique to reconcile net income (from the income statement) to the cash provided by or used in operating activities on a cash flow statement. This method starts with net income and then adjusts for non-cash expenses, non-operating items, and changes in working capital.

By breaking down these adjustments, analysts and investors gain a clearer understanding of the sources and uses of operating cash flow and can better assess the quality of earnings, liquidity, and operational efficiency.

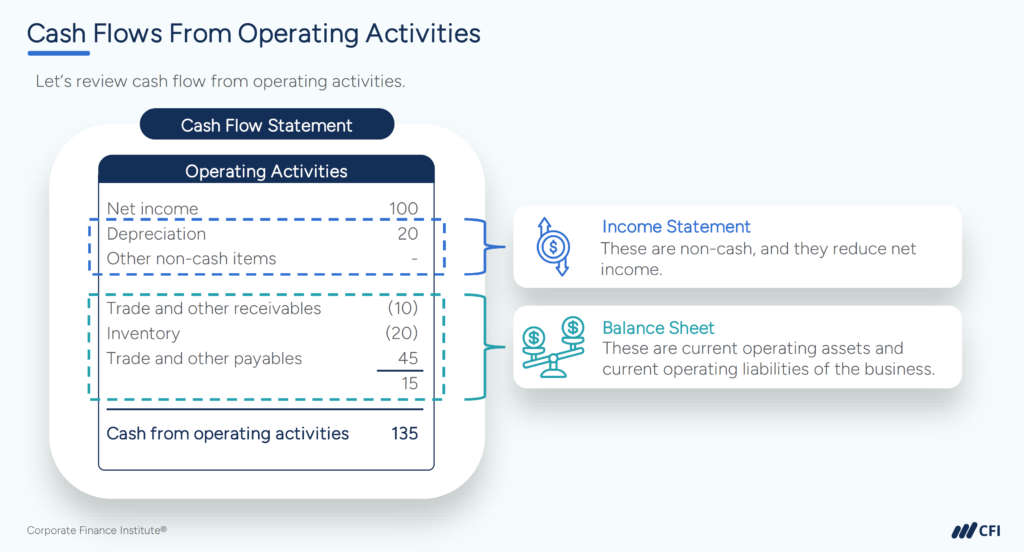

Income statements are prepared using accrual accounting, which includes non-cash items and accounting-related timing differences. Therefore, net income does not reflect actual cash generated by the business. Under the indirect method, you can adjust net income for those non-cash expenses and timing differences to determine actual cash flow for the period.

Non-cash expenses are items that affect net income but do not involve actual cash movement. These items are added back (for expenses) or subtracted (for gains) to reconcile net income to cash flow from operating activities.

Common non-cash adjustments include:

Items that reduced net income but did not use cash:

Gains and losses from financing or investing, such as a gain from the sale of an asset, which do not reflect actual cash related to operations:

Increases or decreases to current assets and liabilities:

This example mirrors the process seen in real-world financial statements and models.

Start by gathering the relevant figures from the income statement and balance sheet. You’ll use these figures to perform the calculation in the table below.

| Step | Amount (USD) |

| Net income | $10,000,000 |

| + Depreciation | +$2,000,000 |

| + Amortization | +$500,000 |

| – Increase in AR | –$3,000,000 |

| – Increase in Inventory | –$1,500,000 |

| + Increase in AP | +$2,200,000 |

| – Decrease in Other Current Liabilities | –$700,000 |

| Net Cash from Operations | $9,500,000 |

Explanation:

Result: Net cash provided by operating activities = $9.5 million.

In this example, net cash from operations ($9.5 million) is $500,000 less than net income ($10 million). This difference occurs because the company invested cash in growing accounts receivable and inventory, which reduced available cash.

Key Points:

The indirect method starts with net income and adjusts for non-cash items and working capital changes. The direct method lists actual cash receipts and payments from operations, such as cash collected from customers and cash paid to suppliers.

Both methods arrive at the same cash flow from operating activities, but the indirect method is more commonly used because it’s easier to prepare from existing financial statements.

Indirect Method:

The indirect method is generally more common in practice because it is much easier and faster to prepare using information already available from the income statement and balance sheet. Most companies and accountants use the indirect method for this reason.

The direct method provides more detailed information about specific cash receipts and payments, but it is less common due to the extra effort required to track and report each cash transaction. Both methods result in the same net cash from operating activities, so the choice is primarily about practicality and efficiency.

The indirect method is a standard accounting technique used in the Cash Flow Statement to reconcile net income (from the income statement) to the actual net cash provided by or used in operating activities. The indirect method links the accrual-based net income figure to the actual cash flow so accountants or analysts can reconcile financial statements.

The indirect method formula begins with net income and adjusts for non-cash items and working capital changes to calculate cash flow from operating activities. You add back non-cash expenses, remove non-cash or non-operating gains, and add or subtract changes in working capital accounts to show the cash generated or used during the period.

The indirect method is more common because the data is readily available from a company’s standard accrual-based income statement and balance sheet. The direct method, in contrast, requires tracking and aggregating every single cash transaction (e.g., cash paid to suppliers, cash received from customers), which is far more time-consuming and labor-intensive.

Projecting Balance Sheet Line Items